Operating a dog daycare involves managing constant physical activity and social interaction between animals, making financial risk a standard part of the business. Because you are responsible for multiple pets at once, dog daycare business insurance is necessary to protect against lawsuits, animal injuries, and third-party property damage. In the absence of an appropriate policy, a single event, e.g., a dog fight or a customer injury, may result in substantial out-of-pocket legal and medical expenses.

This article breaks down the essential coverage types, realistic 2026 cost estimates, and the specific liability requirements needed to keep your facility compliant and protected.

What Is Dog Daycare Business Insurance?

Insurance for dog daycare is a collection of policies intended to protect a business from financial loss. It covers expenses related to dog injuries, bites to third parties, facility damage, employee medical costs, and legal defense fees.

Securing pet daycare business insurance coverage ensures that an accident does not require immediate out-of-pocket payments that could threaten the company’s stability.

Difference Between Business and Pet Insurance

It is important to distinguish between these two products:

- Business Insurance: Protects the business owner and the company from liability and loss.

- Pet Insurance: A health policy purchased by a dog owner for their individual pet’s medical care.

Business insurance does not replace a client’s personal pet policy.

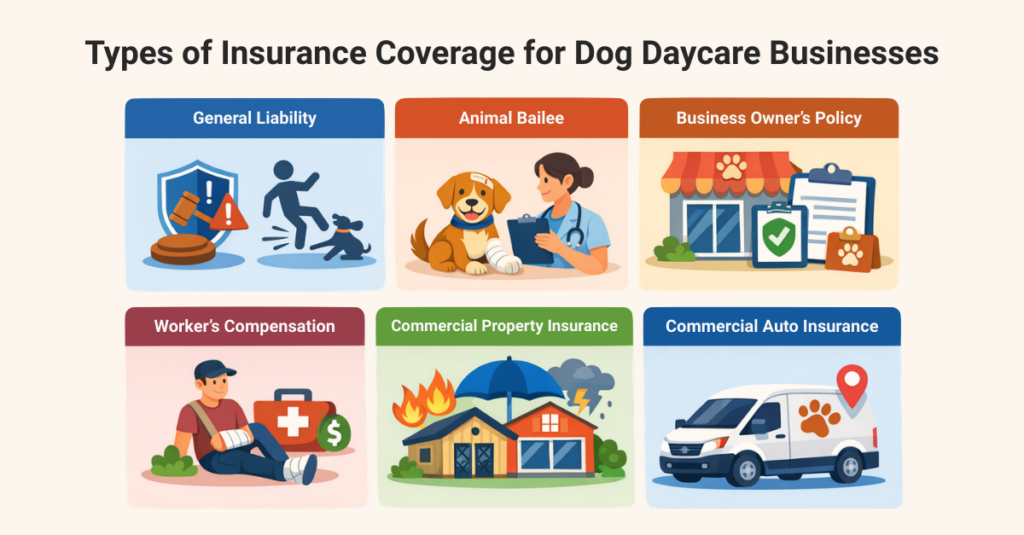

Types of Insurance Coverage for Dog Daycare Businesses

No single policy provides total protection. Most operators combine several specific coverages to address different risks.

General Liability Insurance

This is the standard starting point. It covers third-party claims, such as a client tripping in your lobby or a dog biting a visitor. It manages bodily injury and property damage claims from individuals who are not employees.

Animal Bailee (Care, Custody & Control)

This is a fundamental requirement for dog daycare owners. Standard general liability often excludes property damage currently in your “care.” Because dogs are legally classified as property, you need Animal Bailee to cover veterinary bills or costs associated with a dog’s injury or escape while under your supervision.

Business Owner’s Policy (BOP)

A BOP bundles General Liability and Commercial Property insurance into one package. This is often more economical than purchasing them separately and frequently includes “Business Interruption” insurance, which provides income if a disaster forces a temporary closure.

Workers’ Compensation

Required by law in most states for businesses with employees. This covers medical expenses and a portion of lost wages if a staff member is injured while handling animals.

Commercial Property Insurance

This covers physical resources such as buildings, kennels, grooming equipment, and outdoor fencing, and protects against risks such as fire, theft, or weather damage.

Commercial Auto Insurance

If your business provides transportation services or pet pickups, a personal auto policy will not cover accidents during business hours. A commercial policy is required for vehicle and liability protection during transit.

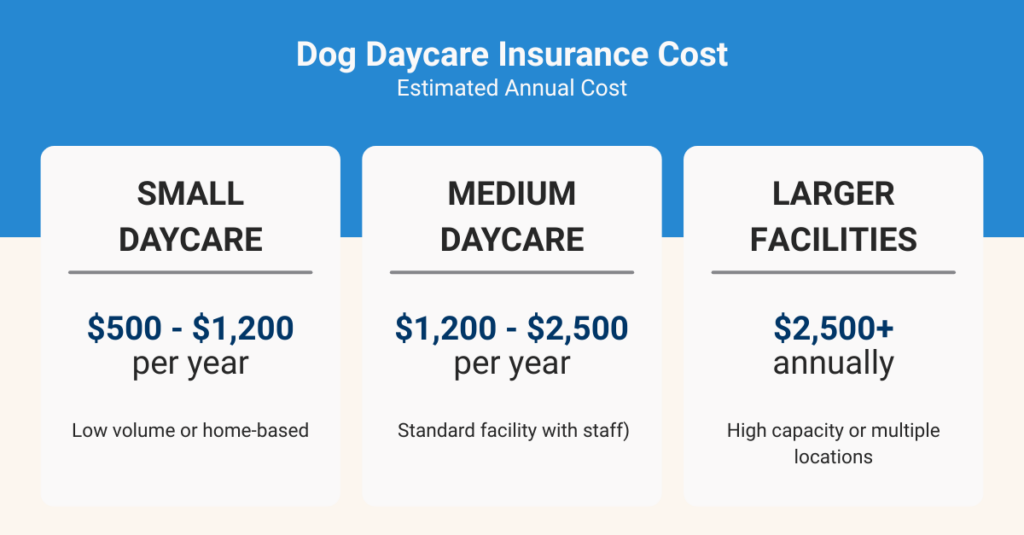

Dog Daycare Insurance Cost (2026 Breakdown)

The estimated insurance cost for dog daycare depends on variables such as facility size, annual revenue, and geographic location.

Estimated Annual Cost

- Small Daycare (Low volume or home-based): $500 to $1,200 per year.

- Medium Daycare (Standard facility with staff): $1,200 to $2,500 per year.

- Larger Facilities (High capacity or multiple locations): $2,500+ annually.

Monthly Cost Estimate

Most operators pay between $50 and $200 per month for a standard insurance package.

What Affects Insurance Cost?

- Number of dogs: The greater the daily capacity, the higher the statistical risk of an incident.

- Number of employees: The more employees, the more the workers’ Compensation premiums.

- Claims history: Previous incidents or lawsuits will lead to higher rates.

- Location: The rates are determined by the local market rates and state laws.

- Coverage limits: Choosing higher limits (e.g., $2 million instead of $1 million) increases the premium.

Dog Daycare Insurance Requirements

Meeting dog daycare insurance requirements is essential for obtaining a business license and staying compliant with state laws. Because you are responsible for public safety and animal welfare, authorities and partners expect specific protection.

Licensing and State Mandates

Licensing requirements vary by state. Many local boards require a Certificate of Insurance (COI) before issuing a permit. Some states specifically require:

- General liability minimum limits: Usually $1 million per occurrence.

- Animal bailee coverage: Protects your pets when they are in your care.

- Workers’ Compensation: It is required by law in most states if you employ workers.

Landlord and Franchise Standards

- Landlords: Most commercial leases require proof of insurance to protect the property owner from lawsuits involving your clients or dogs.

- Franchise brands: These may also require higher coverage limits of $2 million or more to cover the corporate brand and other areas of operation.

Dog Daycare Liability Risks You Must Understand

A dog daycare is a business that deals with unmanaged animals in a communal area. Identifying such risk characteristics is the first step towards limiting them.

- Dog fights: Dogs can injure one another, leading to veterinary bills and potential legal disputes. Without insurance, your business must pay for treatment and compensation.

- Escapes: If a dog escapes and gets injured or lost, the owner may hold your business responsible. This can lead to search costs, vet bills, or legal claims.

- Illness outbreaks: Diseases such as kennel cough that can be transmitted among dogs. In case of wrong health screening and sanitation, its owners can allege negligence.

- Employee negligence: Mistakes such as improper supervision or handling can lead to injuries or escapes. Your business can be held financially responsible.

- Customer injury: Customers visiting your daycare may slip, fall, or get bitten. Medical bills and legal costs can quickly become expensive.

- Property damage: Dogs may damage customer belongings, neighboring property, or your facility. Insurance covers repair and replacement costs.

Financial Consequences of Not Being Insured:

Without insurance, the business owner will bear the legal costs, hospital bills, and settlements. An individual lawsuit or a dog mishap can exceed the liquid assets of most small businesses, resulting in closure.

What Insurers Cover Dog Daycare Companies?

General commercial insurance often excludes animal-related incidents. It is necessary to find providers who understand the risks of the pet industry.

- Pet Care–Specialized Insurers: These companies design policies specifically for daycares, including “Animal Bailee” coverage, which protects the dogs themselves.

- National Carriers: Larger insurers may offer general liability coverage, but often require specific riders to cover animal-related exposures.

- Independent Brokers: They will compare various policies to identify the best coverage for a given facility size and a given list of services.

How to Compare Quotes:

Concentrate on the per-occurrence limit and the aggregate of annual. Make sure that the policy specifically refers to “professional liability” and “animal bailee,” not just to general liability.

How to Choose the Right Dog Daycare Insurance Policy

Use this checklist to evaluate potential policies:

- Verify Coverage Limits: Ensure limits meet your lease requirements and potential risk levels.

- Confirm Animal Bailee Inclusion: This covers injuries to the dogs while they are in your care.

- Review Exclusions: Check for breed restrictions or specific incidents (like off-leash walks) that are not covered.

- Compare Deductibles: Determine if the out-of-pocket cost is manageable in the event of a claim.

Ask About Claims Process: Confirm if the insurer has experience handling pet-related disputes.

Common Mistakes Dog Daycare Owners Make

One of the most common mistakes is purchasing only general liability, which usually covers personal injuries but not the dogs themselves. By ignoring the animal bailee, the business will be responsible for the medical expenses of a wounded pet. The advice to underassign monthly costs and savings may result in no protection during a significant event.

Many owners also forget to update coverage as they grow or add services like grooming. Finally, confusing pet insurance with business insurance is a common mistake; pet insurance covers an individual dog’s health, while business insurance protects the company from liability.

How Software Helps Reduce Insurance Risk

Dog Daycare Management software provides a digital record that is essential during insurance disputes. It allows for incident logging to document the specifics of a scuffle and vaccination tracking to prevent the entry of unprotected animals.

Monitoring behavior can help staff isolate and exclude dogs that do not suit group play, and digital waivers ensure that every client understands the inherent risk of daycare. These devices leave a professional paper trail that shows the business engaged in reasonable safety measures.

Conclusion

Insurance is an essential part of a responsible business plan. While the risks of managing a pack are constant, the right policy ensures that a single accident does not lead to financial ruin. The cost of coverage is manageable compared to the potential loss from a lawsuit. Owners should review their policies annually to ensure coverage remains aligned with the size and scope of their operations.

Frequently Asked Questions

1. Is dog daycare insurance legally required?

While state laws vary, most commercial landlords require liability insurance to sign a lease. Some local licensing boards also mandate coverage for animal-related businesses.

2. What happens if a dog is injured at daycare?

If the business has Animal Bailee insurance coverage, the insurer typically pays for the veterinary treatment. Without it, the daycare owner is personally liable for the costs

3. Does pet insurance cover daycare accidents?

An owner’s personal pet insurance may cover the initial vet bill, but that insurance company may then seek reimbursement from the daycare owner.

4. Can I run a daycare without animal bailee coverage?

It is possible, but highly risky. Most general liability policies specifically exclude damage to property (including pets) that is in your “care, custody, or control.

5. How much liability coverage should a dog daycare carry?

An industry standard is a limit of $1,000,000 per occurrence.

6. Are home-based dog daycares required to have insurance?

Yes. Standard homeowners’ insurance policies generally exclude business activities, meaning a separate commercial policy is needed to protect the owner.